Using data to understand the business opportunity in serving professionals with student loans.

Shur, with our partners, is conducting the deepest consumer data study of professionals with student loans. These insights are built into all our products and services – helping borrowers achieve financial wellness, and our enterprise partners identify new customers and revenue streams within this under-examined population.

Using data to understand the business opportunity in serving professionals with student loans.

Shur, with our partners, is conducting the deepest consumer data study of professionals with student loans. These insights are built into all our products and services – helping borrowers achieve financial wellness, and our enterprise partners identify new customers and revenue streams within this under-examined population.

Shur news & developments.

Milken Global Conference 2024

KB joined a distinguished panel for Moving the Needle Toward Lifetime Financial Security for All.

Profile Piece by Northwestern Mutual

How Kahlil Byrd of Shur Is Focusing on Helping Graduates Move From Student Debt to Wealth

Milwaukee Showcase: NM Black Founder Accelerator

Thanks so much to Northwestern Mutual and gener8tor for the amazing experience as a part of the NM Black Founder Accelerator.

Our work. Our impact.

Through national studies and enterprise partnerships as described in the two case studies below, Shur's expertise is uncovering insights that are creating new pathways to wealth for professionals with student loans and a new prime customer base for financial institutions.

National Study 2021-2022

Since 2021: Largest comprehensive pre- and during-pandemic analysis of student borrower financial wellness.

Shur — in partnership with Equifax® and VantageScore™ — has been conducting comprehensive, national studies of nearly 9 million student loan records to gain a clear understanding of who the student loan borrower is, whose credit scores leave them undervalued, and why.

National Study 2021-2022

Since 2021: Largest comprehensive pre- and during-pandemic analysis of student borrower financial wellness.

Shur — in partnership with Equifax® and VantageScore™ — has been conducting comprehensive, national studies of nearly 9 million student loan records to gain a clear understanding of who the student loan borrower is, whose credit scores leave them undervalued, and why.

National Study 2021-2022

Since 2021: Largest comprehensive pre- and during-pandemic analysis of student borrower financial wellness.

Shur — in partnership with Equifax® and VantageScore™ — has been conducting comprehensive, national studies of nearly 9 million student loan records to gain a clear understanding of who the student loan borrower is, whose credit scores leave them undervalued, and why.

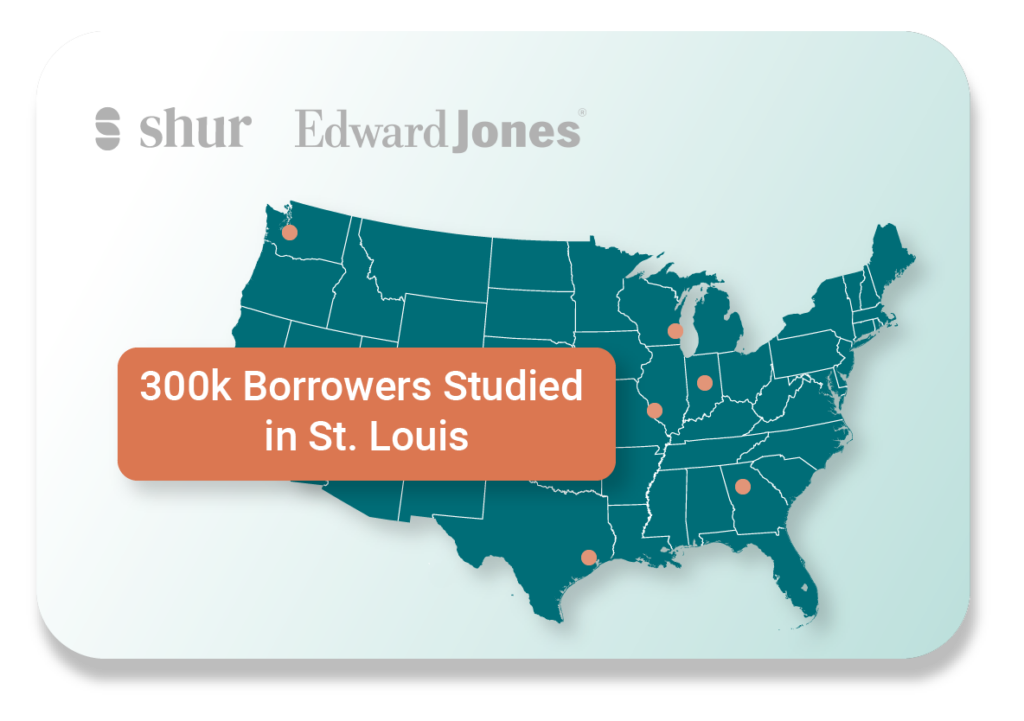

Enterprise Partnership - Ongoing

Since late 2022, Shur partnered with Edward Jones to analyze the financial reality of borrowers in the St. Louis region and beyond.

Edward Jones® is creating what is emerging as a multi-faceted and well-resourced impact experiment focusing on the financial wellness and outcomes for colleagues, customers, and residents living in communities surrounding its headquarters in the St. Louis region. Focusing on the unique challenges of student loan borrowers, Shur is bringing our expertise, platform, data, and financial products to support their vision as we expand to Seattle, Houston, Atlanta, Indianapolis and Milwaukee.

Enterprise Partnership - Ongoing

Since late 2022, Shur partnered with Edward Jones to analyze the financial reality of borrowers in the St. Louis region and beyond.

Edward Jones® is creating what is emerging as a multi-faceted and well-resourced impact experiment focusing on the financial wellness and outcomes for colleagues, customers, and residents living in communities surrounding its headquarters in the St. Louis region. Focusing on the unique challenges of student loan borrowers, Shur is bringing our expertise, platform, data, and financial products to support their vision as we expand to Seattle, Houston, Atlanta, Indianapolis and Milwaukee.

A more complete picture using data.

A decade of data and insights to understand student borrowers’ financial realities.

Methodology: With Equifax® and VantageScore™ — examined the financial dynamics of 896,157 anonymized student loan holders. This is from a 1% sample of the national population, from 2010 and 2015-2019. During these years, this sample of student borrowers had a combined 8,980,378 student loan records.

We sought to understand a variety of crucial factors: How much debt they held and what their payments were; where and for how long borrowers went to college and their graduation rates; the impact on a person’s VantageScore 4.0™ credit scores; data available on ethnicity, gender, household income, and geography.

2.2% of loans fell into default with an average defaulted loan of $6,913. A monthly payment of around $75. (2015-2019)

In 2020, Pew Charitable Trusts reported that many “off track” borrowers stumbled early in loan repayment. Most talked to their loan servicers only after they missed their first payment. Source

The default rate for loans less than $2,000 was 182% higher than for loans exceeding $10,000. (2019)

In 2017, the Center for American Progress (CAP) pointed to media narratives portraying borrowers in default as borrowing more and retaining higher balances. Both CAP and the Brookings Institution (2018) reported that in reality defaults are highest among students who borrow relatively small amounts. Source Source

Students who withdraw from school have a 338% higher default rate than those who graduate from four-year colleges. (2015-2019)

In 2015 and 2018, the Urban Institute pointed out that non-completers tend to make less money and can be demotivated to pay back the debt incurred while in school. Source

2.2% of loans fell into default with an average defaulted loan of $6,913. A monthly payment of around $75. (2015-2019)

In 2020, Pew Charitable Trusts reported that many “off track” borrowers stumbled early in loan repayment. Most talked to their loan servicers only after they missed their first payment. Source

The default rate for loans less than $2,000 was 182% higher than for loans exceeding $10,000. (2019)

In 2017, the Center for American Progress (CAP) pointed to media narratives portraying borrowers in default as borrowing more and retaining higher balances. Both CAP and the Brookings Institution (2018) reported that in reality defaults are highest among students who borrow relatively small amounts. Source Source

Students who withdraw from school have a 338% higher default rate than those who graduate from four-year colleges. (2015-2019)

In 2015 and 2018, the Urban Institute pointed out that non-completers tend to make less money and can be demotivated to pay back the debt incurred while in school. Source

Student loan borrowers with a credit score above 720 (Prime) have a default rate of .1%, with a median payment of $227. While borrowers with credit scores below 579 (Sub-Prime) have a 7.9% default rate with a median payment of $99. (2019)

In 2015, the Federal Reserve Board pointed to both degree non-completion and a borrower’s credit score prior to loan origination as highly predictive of later delinquency in repayment. More so than debt level. Source

Student loan borrowers with a credit score above 720 (Prime) have a default rate of .1%, with a median payment of $227. While borrowers with credit scores below 579 (Sub-Prime) have a 7.9% default rate with a median payment of $99. (2019)

In 2015, the Federal Reserve Board pointed to both degree non-completion and a borrower’s credit score prior to loan origination as highly predictive of later delinquency in repayment. More so than debt level. Source

Where gender was reported, 58% of student loan borrowers captured in our study were women. Women in our sample defaulted at a higher rate than men: 2.4% vs. 2.1% (This is 14.3% higher). (2015-2019)

In 2017 and 2021, the American Association of University Women reported that women assume more student loan debt than men and pay more slowly over time. They cite a combination of less family support, the gender pay gap in and out of school, and — paradoxically — the fact that women are more likely to complete college than men. Source Source

At 4.4%, Black student borrowers have the highest student loan default rate — 220% higher than average. Black borrowers accounted for 8.2% of those with available ethnicity data. (2015-2019)

In 2019, Brandeis University researchers found that after 20 years, Black student borrowers had paid only 6% of their loans while white borrowers had paid off 95% of their outstanding student debt. Source

Where gender was reported, 58% of student loan borrowers captured in our study were women. Women in our sample defaulted at a higher rate than men: 2.4% vs. 2.1% (This is 14.3% higher). (2015-2019)

In 2017 and 2021, the American Association of University Women reported that women assume more student loan debt than men and pay more slowly over time. They cite a combination of less family support, the gender pay gap in and out of school, and — paradoxically — the fact that women are more likely to complete college than men. Source Source

At 4.4%, Black student borrowers have the highest student loan default rate — 220% higher than average. Black borrowers accounted for 8.2% of those with available ethnicity data. (2015-2019)

In 2019, Brandeis University researchers found that after 20 years, Black student borrowers had paid only 6% of their loans while white borrowers had paid off 95% of their outstanding student debt. Source

Our findings cited above focus on borrowers who took loans to attend four-year, nonprofit, public and private institutions of higher education.

We chose 2010 and 2015-2019 for two reasons:

1) We studied borrowers and loans from before the 2020 COVID-19 emergency relief for federal student loans — a suspension of payments and interest — implemented as part of the American Rescue Plan Act. This provides a more accurate representation of the actual student loan system. 2) We studied borrowers and loans after the Financial Crisis of 2007-2008. Significant changes to the system were ushered in by the Health Care and Education Reconciliation Act of 2010, which ended the Guaranteed Student Loan Program. Equifax is a registered trademark of Equifax Inc.